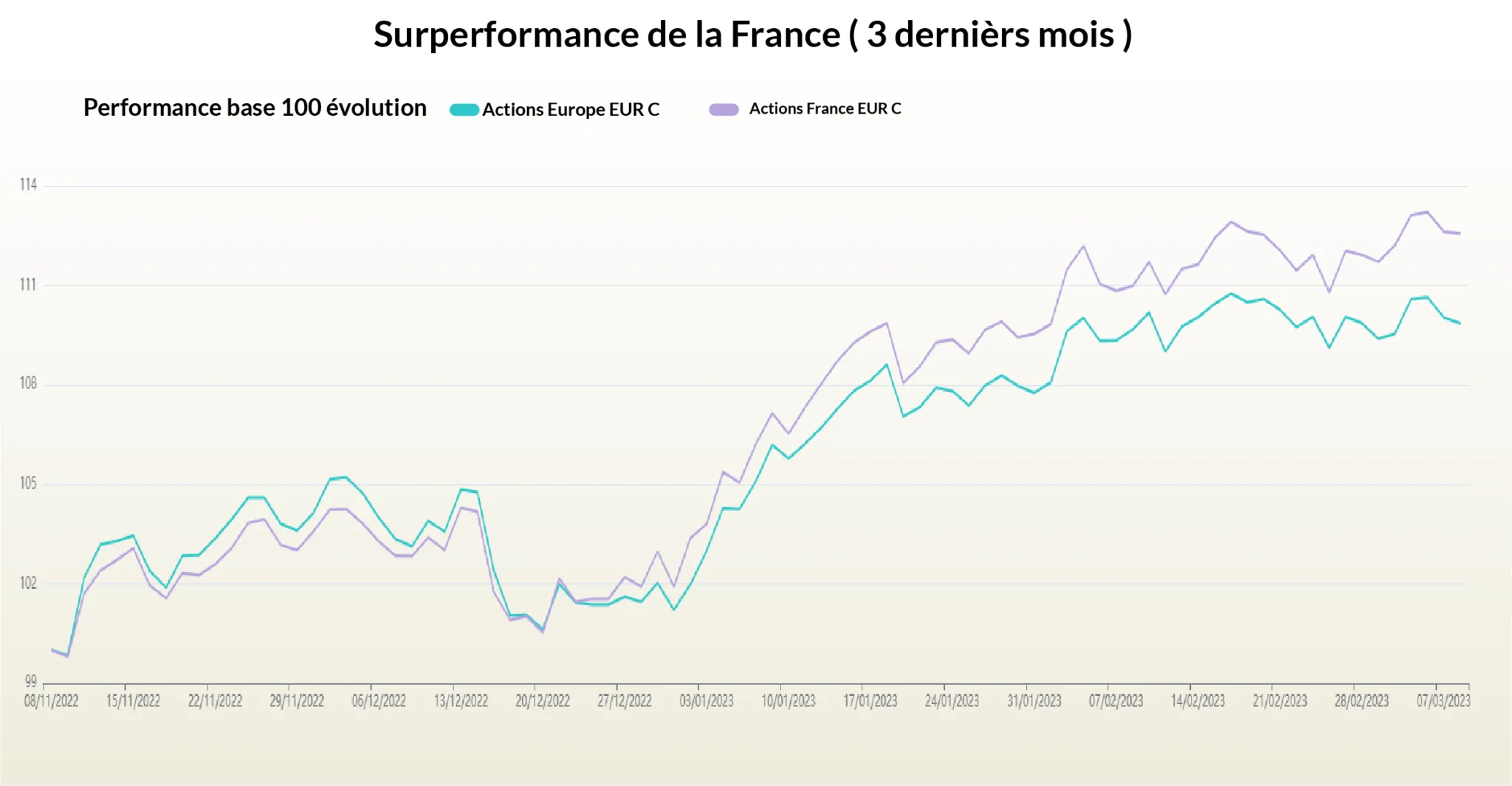

Overview

During the inflationary shock in 2022, France equity funds were not more penalized than the European average. However, they have been significantly more responsive in the equity market rebound that began several months ago.

This outperformance comes from the predominance of services, export-oriented, and energy sectors in the economy and on the country’s equity market.

These sectors are more resistant to inflation than traditional and technology industries.

Indeed, the services sectors in France account for 80% of the working population vs 75% on average in Europe.

Export-oriented sectors such as Luxury and energy represent a significant weighting in French equity indices.

France is therefore particularly better positioned in these sectors than Germany and the Nordic countries, which are more dependent on traditional or technology industries.

Current Situation

The Eurozone Services PMI, an indicator of the business climate in services sectors, showed a better trend. Furthermore, the reopening of China primarily improves the outlook for luxury and tourism. Finally, rising commodity prices continue to support companies specializing in these raw materials.

Scenarios

Positive

Core inflation persists but remains stable around the current level without pushing the ECB to react. The ECB does not need to accelerate its rate hikes to the point of threatening labor market dynamics.

Negative

Core inflation escapes central banks’ control, leaving them no choice but to accelerate their rate hikes. This triggers a recession in developed countries, including France.

Past performance does not guarantee future results. The content above does not constitute investment advice. It is an objective analysis of financial information.