Corporate Bonds Category

Overview

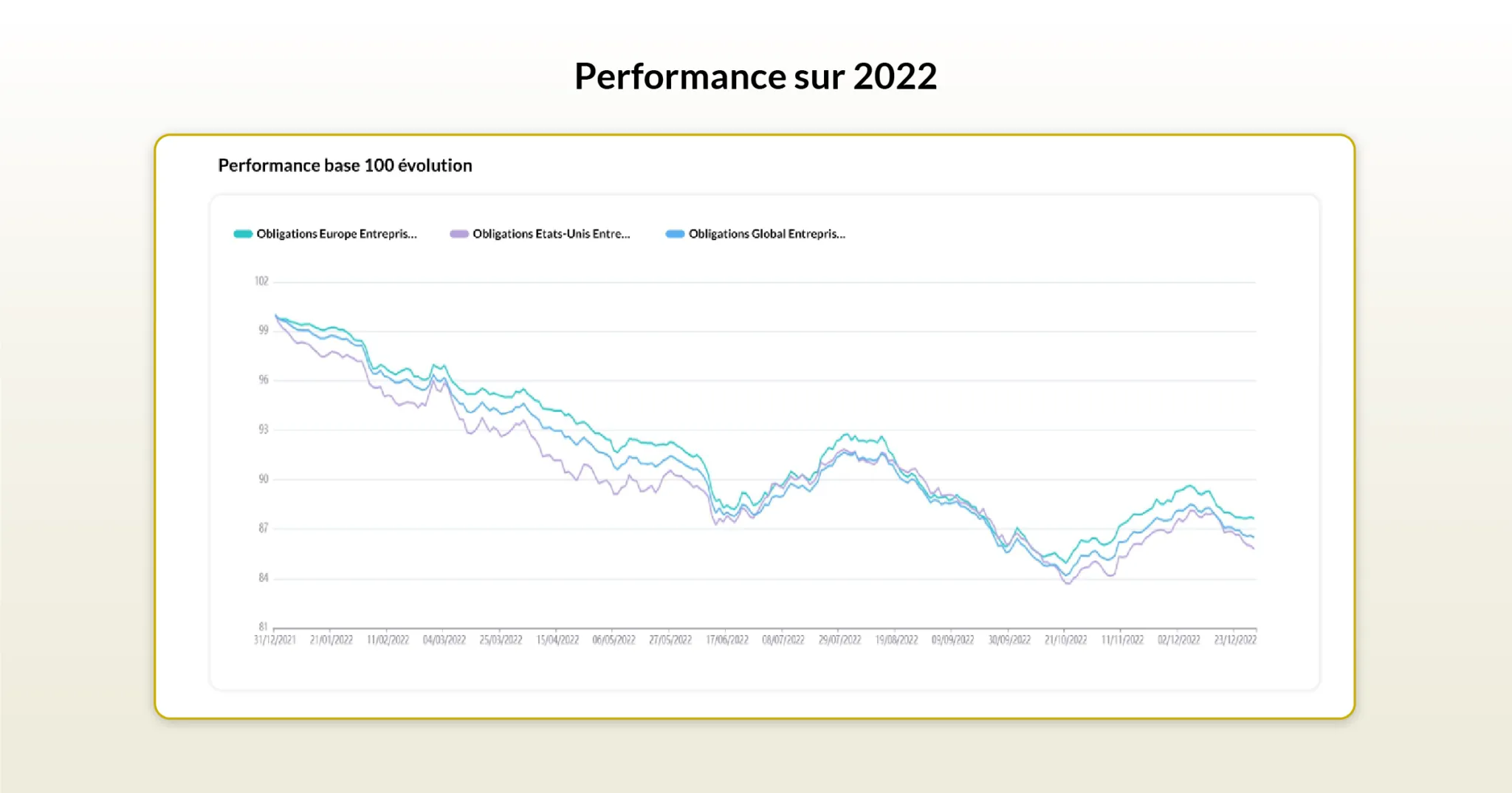

- First, last year was one we had not experienced in nearly 30 years.

- Since China’s closure due to its Zero Covid policy, the surge in commodity prices driven by the war in Ukraine triggered a spike in inflation.

- As a result, central banks were forced to rapidly raise their key interest rates to combat unexpected inflation.

- Clearly, this paradigm shift caused a bond shock, a phenomenon similar to the bond crisis of 1994.

Current Situation

- However, the slowdown in rate hikes by the ECB and the FED signals the approaching end of restrictive monetary policy.

- Indeed, the mention of the term “Disinflation” by FED Chairman Powell has led to expectations of easing inflationary pressures in the medium term.

Possible Scenarios

Base Case

Certainly, the decline in inflation already observed could be amplified by certain events.

These include: the reopening of the world’s factory, the end of fiscal stimulus policies in Europe and the United States, recessionary expectations, and the stabilization of commodity prices.

Moreover, with central banks slowing the pace of key rate hikes, long-term rates could stabilize or even decline.

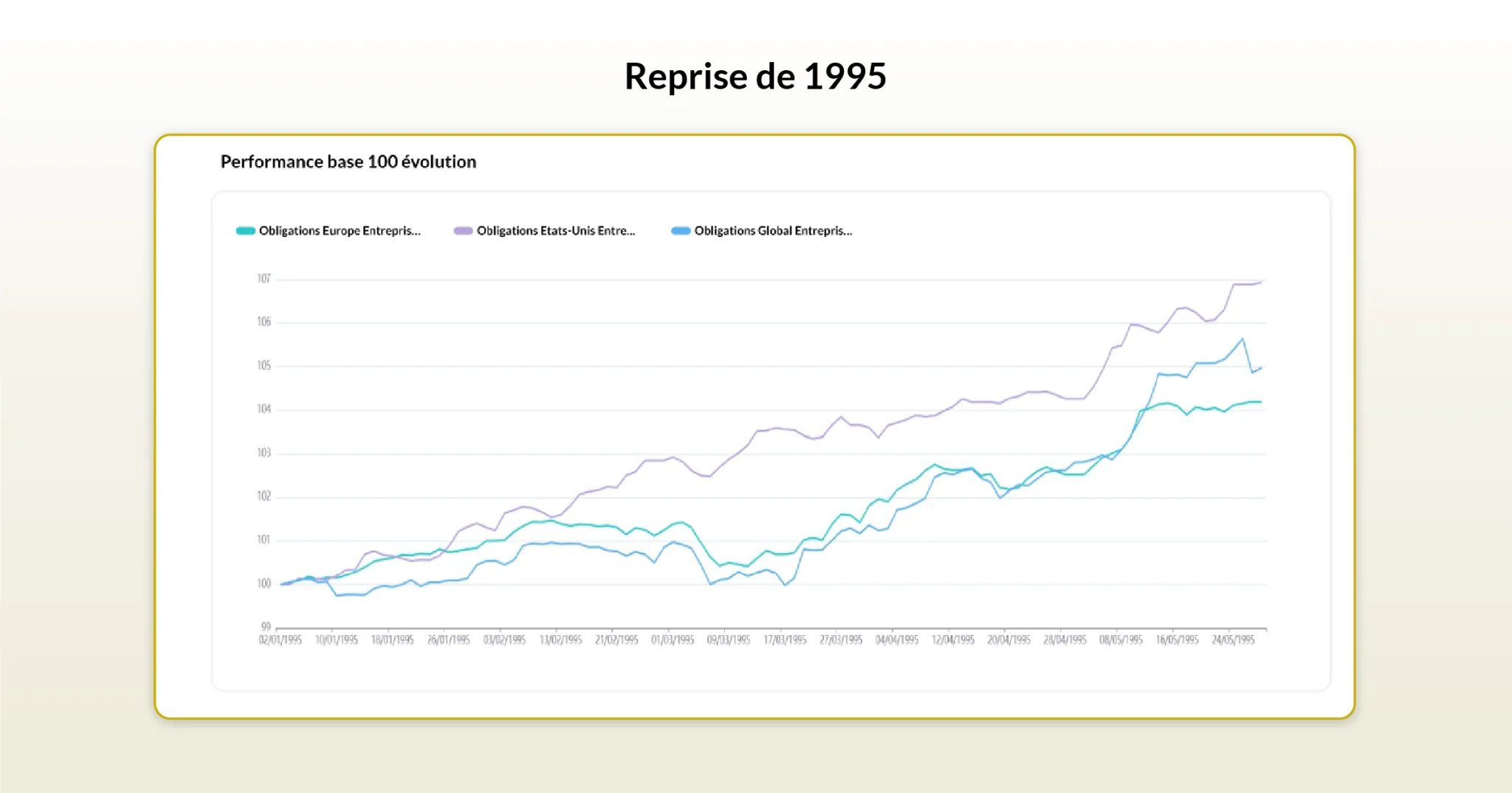

This is what happened in 1995, when a global growth slowdown following the great inflationary scare of 1994 created the bond rally.

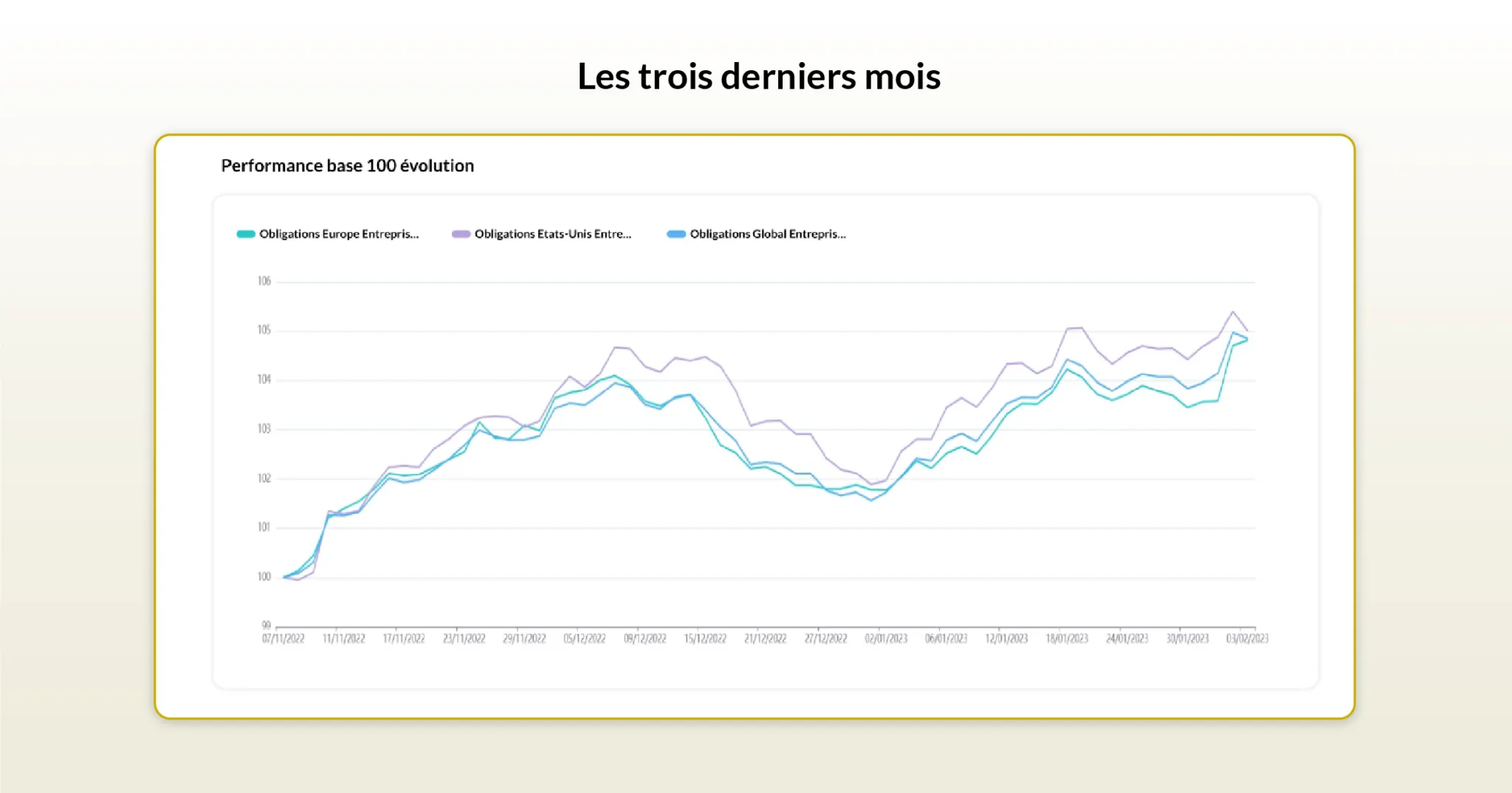

Indeed, this scenario already appears to be underway when looking at the performance of corporate bond funds over the last 3 months:

Indeed, the US Corporate Bonds EUR category seems to be the most compelling to play this scenario.

Undoubtedly, this category suffered more than its “Europe” & “Global” peers during 2022.

Given that current macroeconomic conditions are more favorable, the catch-up effect could be more significant, which would be similar to the 1995 rebound.

Pessimistic

Currently, two factors could derail the base case scenario:

- The Chinese government reverses its reopening policy, leading to a rise in global production costs.

- If an escalation of violence in the Russia-Ukraine conflict drives up commodity prices.

In this scenario, inflation escapes central bank control and recession sets in, leading to a period of stagflation.

During this period, consumption and savings capacity would be reduced, resulting in a decline in both equity and bond markets.

Past performance is not indicative of future results. The content above does not constitute investment advice. It is an objective analysis of financial information.