Global High Yield Bonds Category

Overview

- The year 2022 was unprecedented due to the violence of the inflationary shock; the rate hikes and the bond crash that followed had not been seen since 1994

- In 2023, this bond crash pushed the banking system toward major failures not seen since the subprime crisis

- Inflation is stabilizing but remains elevated; the bulk of rate hikes is probably behind us, but further increases are possible

Current Situation

However, the equity market is reaching all-time highs, particularly in France. Yet various indicators, such as the yield curve inversion, suggest that a sharp slowdown or even a recession could occur by the end of 2023. In this context, the risk/return profile of the equity market appears to lean more toward risk than toward return expectations.

In this environment, the global high yield bonds category seems well-suited to deliver an attractive return with lower risk than equities. Indeed, in a low-growth or moderate recession economy, this category benefits from its corporate exposure to offer an attractive yield and volatility similar to the bond market. This is attributable to high yields and a low default rate, provided we do not enter a significant recession.

Scenarios

Optimistic

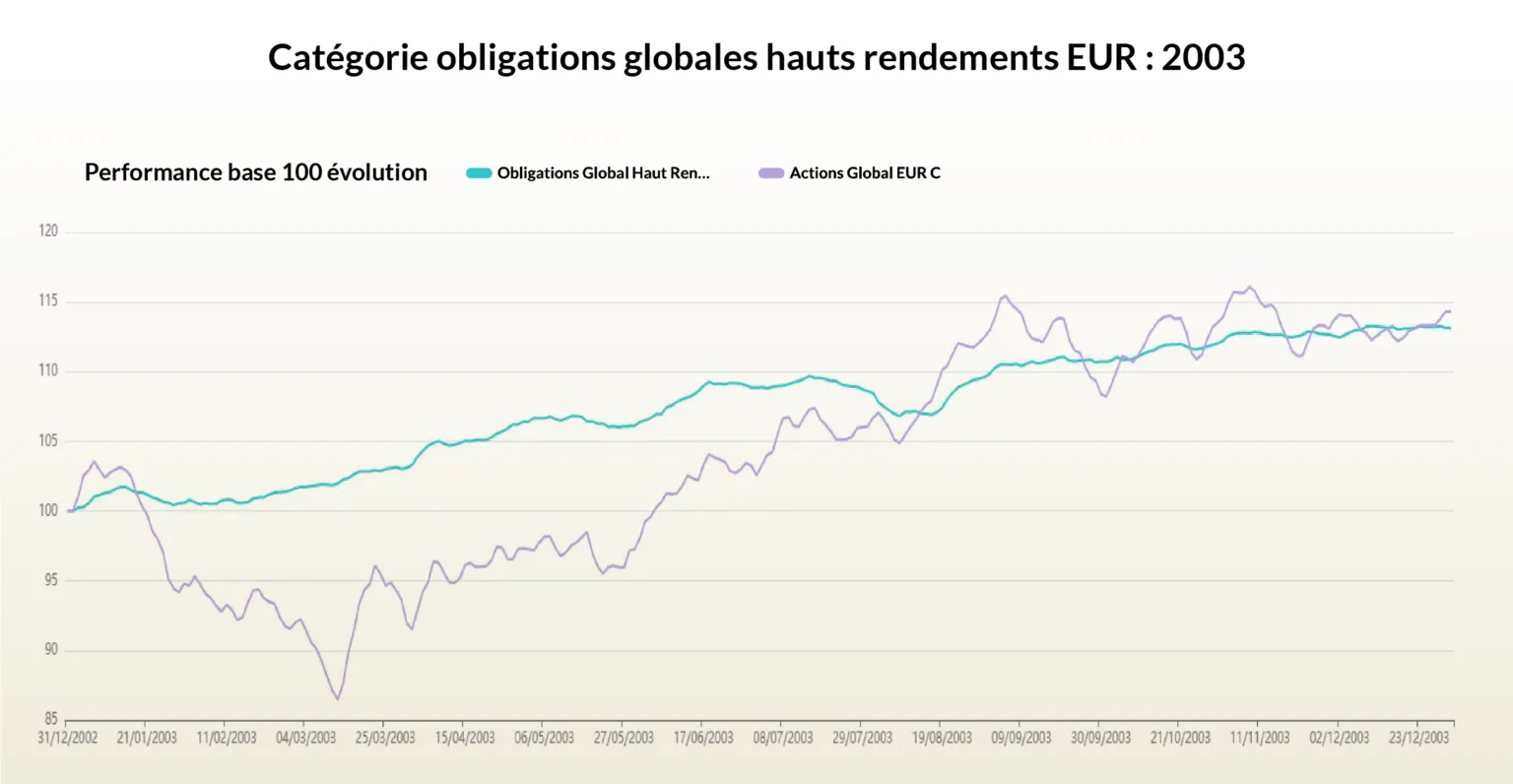

Following the stabilization of inflation at the beginning of the year, it should gradually decline thanks to moderate rate hikes implemented by central banks. In this scenario, we could experience growth close to zero. This context is reminiscent of 2003, when moderate growth was observed globally and particularly in France, with growth below 1%.

Thus, the global high yield bonds category offers a return similar to equities with significantly lower volatility and maximum drawdown.

Pessimistic

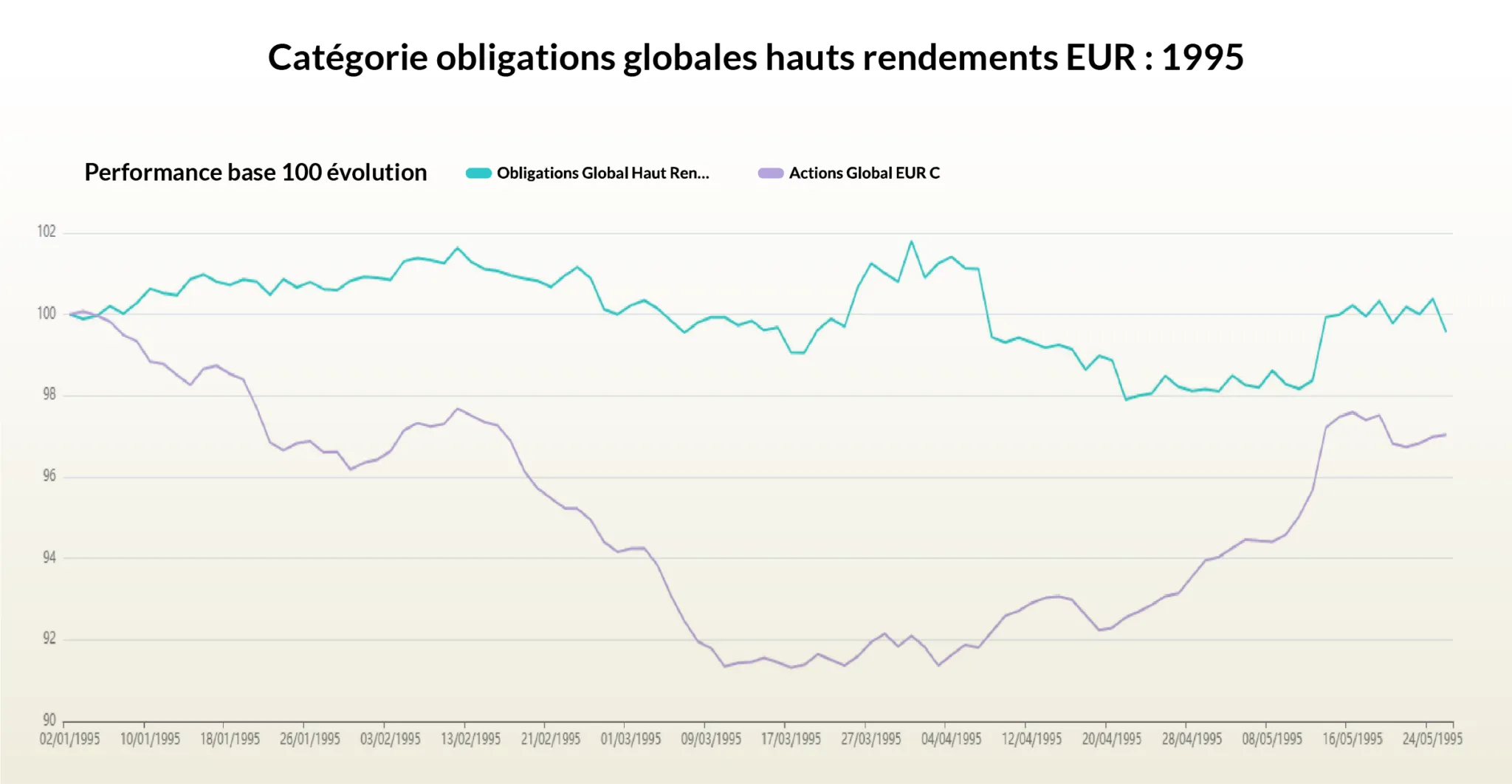

Inflation stabilization would continue thanks to sustained central bank intervention. This would cause a moderate recession in the global economy, weighing on corporate earnings. This scenario corresponds to what we experienced in 1995. During that period, central banks maintained high rates to stabilize inflation, which weighed on borrowing capacity for economic actors and triggered a moderate recession.

In this scenario, we can observe that the global high yield bonds category delivers better returns than the global equities category, with significantly lower volatility and maximum drawdown.

Past performance is not indicative of future results. Fees are included in performance figures. The content above does not constitute investment advice. It is an objective analysis of financial information.